How do exchange funds work? The ultimate guide

What you'll learn

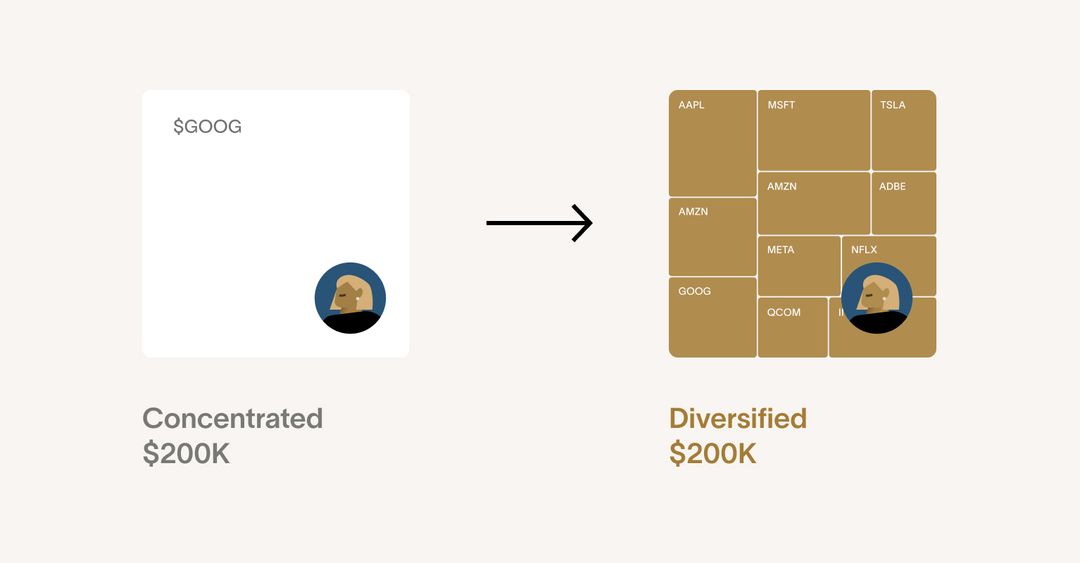

If you possess a significant stock position and maintain a long-term investment horizon, exchange funds represent a tax-efficient method for diversifying your portfolio. These funds enable you to combine your stock with that of other investors who hold concentrated positions in different stocks, forming a communal fund. By exchanging your stock for shares in the fund instead of conducting individual sales and diversifications, you and other investors can diversify your portfolios while deferring capital gains taxes simultaneously.

By mitigating both your risk and the tax drag associated with selling stock, an exchange fund can significantly contribute to achieving your long-term investment objectives. But what precisely is the mechanism behind an exchange fund, and how does it impact your overall investment strategy? This article aims to demystify all the intricate details for you.

If you prefer a broader overview, you may find it beneficial to begin with our introduction to what an exchange fund entails.

The underlying issue many investors face

When you find yourself in possession of a stock position that has experienced considerable appreciation, it's wise to mitigate risk. Typically, financial planning literature advises restricting exposure to any single stock to less than 10% of your net worth.

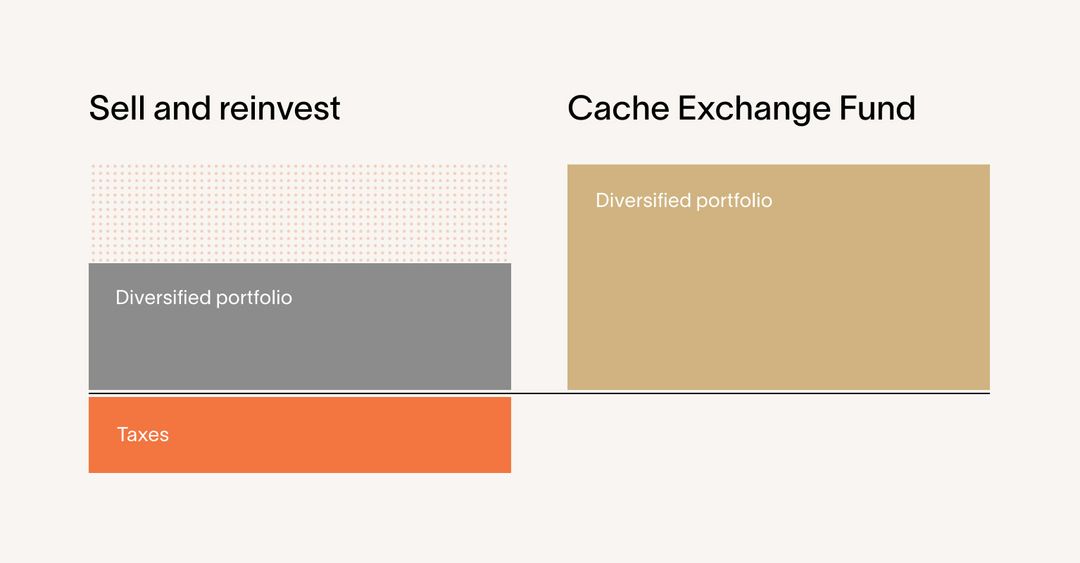

To mitigate this concentration risk, the common advice you'll often encounter is, "You should sell and diversify." Consequently, most investors follow suit: They sell their concentrated position, settle the capital gains tax, and diversify into an index fund. However, selling appreciated stock can result in a substantial tax liability that nullifies years of portfolio growth. Hence, it's understandable why some investors opt for retaining a concentrated position rather than enduring the tax drag on their portfolio. Taxes rank as the primary reason individuals hold onto concentrated stock positions.

Handling a concentrated stock position can seem like a lose-lose scenario – you either retain excessive risk or face a substantial tax liability.

Enter the exchange fund

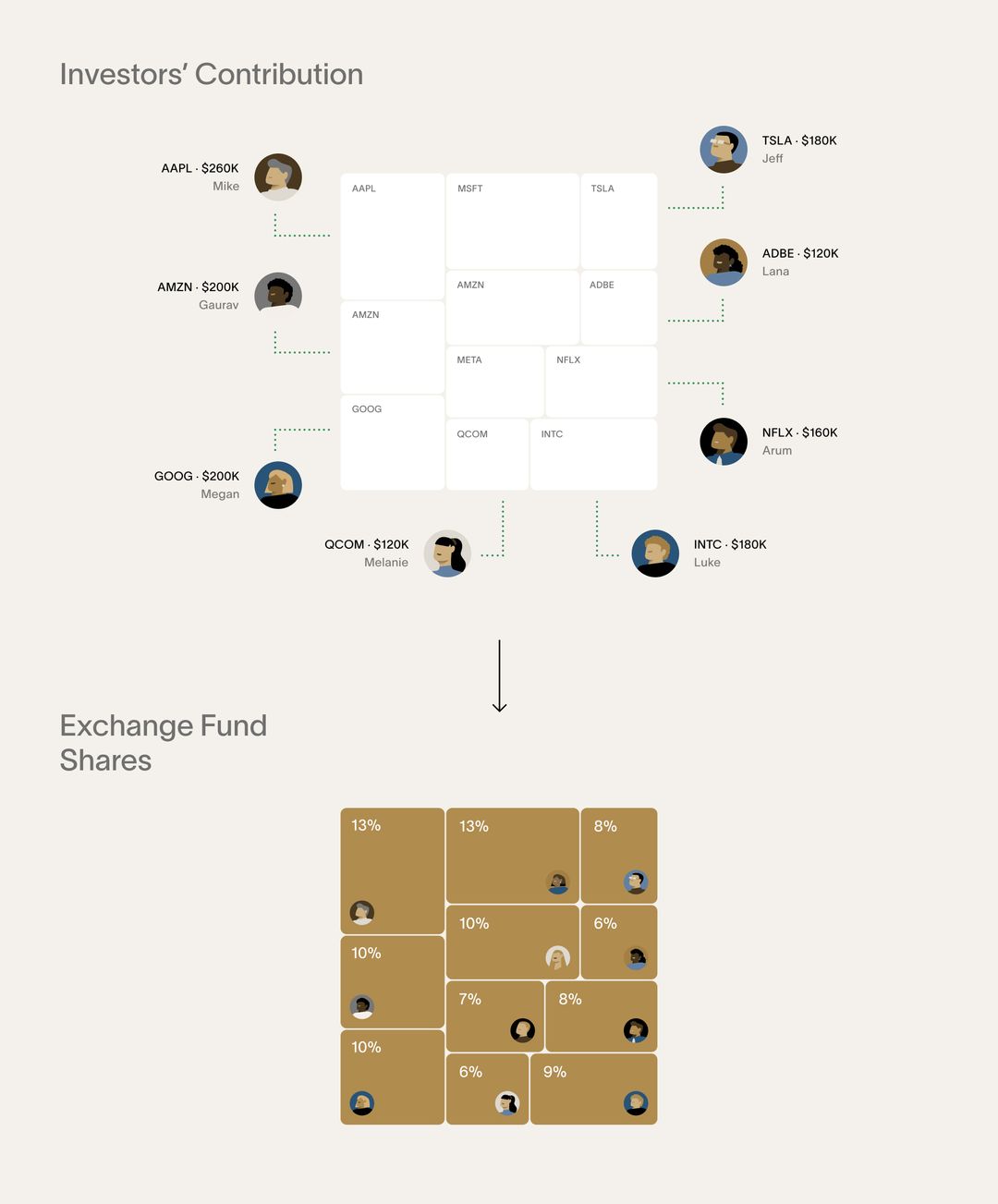

Exchange funds represent a category of private funds capable of providing tax-efficient diversification by bypassing the "sell" component of the sell-and-diversify strategy. To accomplish this objective, an exchange fund aggregates stocks from various shareholders in predetermined quantities to align with a specific blend, such as a stock market index.

Since you exchange your stock for fund shares, you (and all the other investors) are diversified by virtue of participation.

Following a seven-year curing period, you have the option to withdraw a diversified basket of stocks from the fund. Presently, the tax code regards contributions to – and redemptions from – qualifying exchange funds as non-taxable. This implies that you can diversify your concentrated position without experiencing tax drag. Instead, your taxes are deferred until you opt to sell the assets withdrawn from the fund, and the cost basis from your original stock remains unchanged.

The sell-and-diversify approach has historically been favored over participating in an exchange fund for several reasons, with one of the primary factors being the lack of availability of exchange funds until relatively recently for most investors.

The history of exchange funds

Exchange funds indeed have a long history, dating back to the establishment of Section 351 Exchanges in the 1930s within the tax code. Moreover, provisions for "like-kind" exchanges have existed, exemplified by the 1031 Exchange introduced in 1954 to enable real estate investors to defer taxes during property exchanges.

Exchange funds are provided by reputable investment firms such as Goldman Sachs and Morgan Stanley. They have been available institutionally since the 1960s, gaining broader acceptance after Eaton Vance (now part of Morgan Stanley) secured an IRS ruling in 1975 permitting their use. Despite common misconceptions, firms like Vanguard and Blackrock do not currently offer exchange funds.

Exchange funds have historically been geared towards ultra-wealthy investors, primarily accessed through private wealth channels, which has led to their limited general awareness. They often only come into the public eye when the financial affairs of wealthy individuals are scrutinized, such as in the case of Mitt Romney during the 2012 presidential election, as highlighted in a New York Times piece. Even today, a Google search for "exchange funds" predominantly returns results related to similarly named "exchange-traded funds" (ETFs).

Indeed, there has been a notable shift. Previously, exchange funds were exclusively available to "Qualified Purchasers" with over $5,000,000 in investment assets. Traditional providers typically required hefty minimum investments ranging from $500,000 to $1 million. However, in 2023, our company introduced the Cache Exchange Fund, extending eligibility to accredited investors with reduced investment minimums and fees, thereby broadening accessibility to a significantly larger audience.

What rules apply to exchange funds, and who can participate?

Although exchange funds offer numerous advantages, they are geared towards long-term investment and are accessible only to specific investors. These fundamental guidelines govern investor eligibility, the length of their involvement, and the types of assets the fund can include.

-

Investor Eligibility

Exchange funds are private funds for sophisticated investors who are capable of understanding their benefits and risks. As such, they are only available to Accredited Investors – which means individuals who earn:

- Over $200,000 per year or

- Couples earning over $300,000 per year, or.

- Households with a net worth over $1 million (excluding the value of their primary residence)

As we mentioned in the history of exchange funds, participation used to be limited to Qualified Purchasers with more than $5 million, however the Cache Exchange Fund is available to Accredited Investors as well.

-

Stock Eligibility

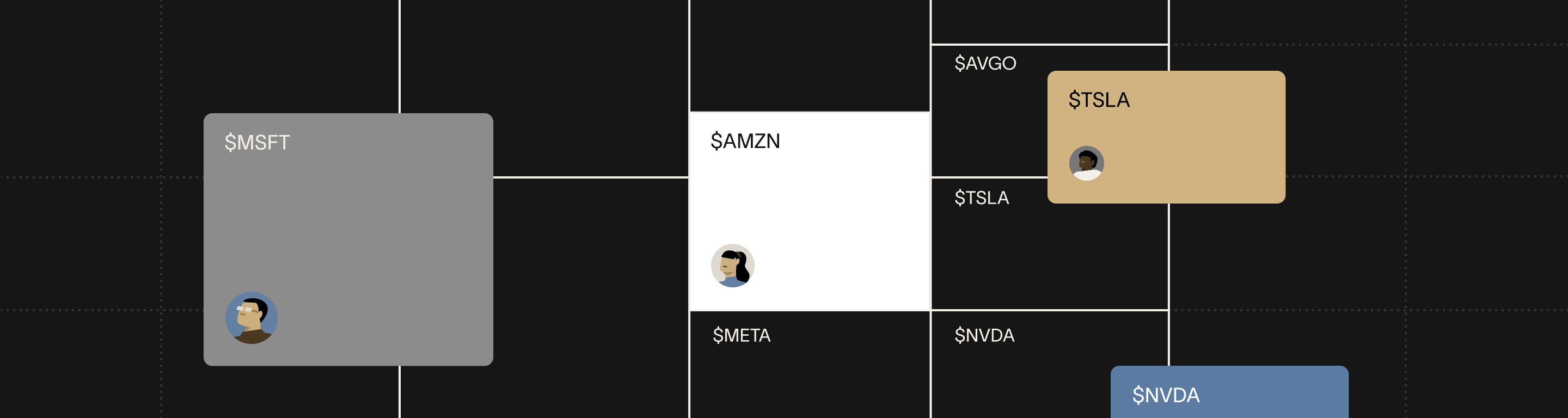

Exchange funds accept stocks that allow them to achieve the right balance to meet their investment objectives. For example, The Cache Exchange fund is set up to approximate the holdings of the Nasdaq-100 index. That means there can be a supply and demand problem when stocks you hold are oversubscribed because too many other investors want to bring in the same stocks. That means a given fund might not accept your stock, or it might need you to wait until it finds other investors to balance your holdings. See the timeline below to understand how this works.

-

Fund Structure

Each fund is structured as a limited partnership (usually a Delaware LLC). Each contributing shareholder receives a pro-rata share of the entire portfolio in the form of fund shares.

-

Illiquidity requirement

The fund must hold 20% of its assets in qualifying illiquid assets, such as real estate or commodities. Generally, real estate assets are used to fulfill this tax code requirement because they often produce income that can help the fund meet its investment objectives and potentially provide additional returns.

-

Holding period

Although you achieve diversification as soon as you put your stocks into an exchange fund, the current tax rules mandate that each investor remains in the fund for seven years before they can withdraw a tax-deferred basket of stocks from the fund. Early withdrawal can result in the loss of that tax deferral, and you may incur fees or penalties with your fund provider. Depending on the provider, exchange funds may also have a multi-year lockout when the fund is created.

How does the seven-year rule work?

So, why is there a seven-year holding period with exchange funds, and what happens if you need to exit before the seven years have passed?

The seven-year rule is a product of the current tax code. In many types of exchanges that let investors defer capital gains taxes, there is a minimum holding period. These minimums are meant to ensure that the transaction is truly an exchange and not a sale in disguise.

This law review article explains the legal mechanics in detail, but the takeaway is that the seven-year holding period is something you’ll need to plan for. There are several consequences if your circumstances change and you need to withdraw from an exchange fund early. To meet their investment objectives, most exchange funds have a lockout period during their first few years, so it could be three years or more until you can access your assets. Once the lockout is over, you’ll be able to withdraw either assets equivalent to your share of the fund (based on its current-day net value) or the current-day value of the shares you contributed – whichever is less. Your provider may also charge fees.

Timeline: How an exchange fund works

Unlike an ETF or mutual fund, exchange funds are not ready for investment continuously. They open to contributions at periodic intervals when sufficient diversity of demand exists. Once a fund manager has identified participants with the right mix of stocks to achieve the fund’s objectives, there is an escrow-like period leading up to the fund’s closing. Then the fund is created and its manager administers it for at least seven years when tax-deferred withdrawals become available – and potentially beyond. Here are detailed timelines that show you what you can expect from the process if you indicate interest and participate in an exchange fund.

-

Raise your hand

months before fund creation

Indicate your interest in contributing some or all of your large stock position to the fund. Exchange funds are constantly balancing supply and demand, and they might be open or oversubscribed on certain stocks. It could be several months until a fund that can accommodate you is created.

-

Get your invitation

one month to go

Once fund managers have interest from enough investors to meet the fund’s objectives, they invite investors to join the fund. They’ll let you know how much of your holding the fund can take, they’ll share relevant fund documents, and they’ll ask you to accept your allocation.

-

Verify your eligibility

less than one month to go

You’ll verify your accreditation status by sharing information about your net worth or income. Your identity will also be verified through KYC/AML checks, and you’ll be asked to share information about your tax status.

-

Move stocks to reserve

less than one month to go

Once you’ve accepted the invitation, you’ll move stocks from your existing brokerage to a reserve account (or escrow account) where it will be held until the fund closes.

-

Sign subscription documents

less than one month to go

The fund manager will share the full set of terms for you to review and sign, making your participation in the fund official.

-

Final inspection

three days to go

Prior to the close, a final inspection of the intended close will be presented to you. Details about the real estate investment are finalized and presented within this information.

-

Closing

one day to go

The fund will close on a preset closing date. When it closes, the net asset value is calculated based on the value of the shares upon market close that day.

-

Receive your fund shares

Your fund shares are issued on a pro-rata basis, as determined by the net asset value of the fund and the value of the shares you contributed. You are officially diversified!

How fund participation works

Once the fund is set up, there are a few notable milestones before you can redeem your shares in the fund for a tax-deferred basket of stocks. These are the stages you’ll encounter throughout the lifecycle of your investment:

If you want to receive the benefits of an exchange fund, you have to commit to it. Redemption requests after the lockup but before the seven-year mark are satisfied by distributing some or all of your original contribution back to you. Specifically, you’ll receive the lesser of:

- The value of the stock you contributed, calculated at the time of redemption or

- The value of your share in the exchange fund, based on the fund’s current net asset value.

Basing the withdrawal amount on the lower-valued item prevents participants from gaming the system if, for example, the stock they initially contributed outperforms the rest of the portfolio. Early redeemers may also incur fees from their providers.

For what it’s worth, this seven-year requirement is significantly shorter than some other alternative tax-advantaged investments. Charitable trusts’ are usually structured as a 20+ year holding period. Depending on your age, an IRA or 401(k) might require up to 40 years before you can withdraw your investment without penalties.

After seven years, you can request to withdraw your share of the fund. The fund manager will distribute a diversified basket of 15 to 25 stocks that match your ownership percentage, and your cost basis from the stock you initially contributed will carry over (allowing for possible optimizations if there are opportunities for tax-loss harvesting within the distributed basket).

There is not a “sale” at this point, so no taxes will be due. And there are no fees associated with redemption.

Keep in mind that there’s nothing forcing you to redeem at the end of seven years. Cache Exchange Funds, for example, are perpetual-life vehicles, which means they will continue to grow in a tax-deferred manner for as long as you wish to participate. You can also roll over your redemptions to another exchange fund.

The ability to remain in the exchange fund beyond seven years can help facilitate longer-term tax planning. You may want to wait until you have less income (and a lower tax rate). Or you may want to pass your share of the fund on to your heirs upon your death – under current tax rules, the cost basis could reset at that point.

Any dividends that are received from the stocks in the fund are additive to the fund’s balance sheet. The cash that is generated from dividends (or from the fund’s real estate investments, stock lending, etc.) will primarily be used to help achieve the fund’s investment objective through various portfolio management techniques. Fund income is generally distributed to investors on a discretionary basis.

If you redeem your share of an exchange fund after seven years, your cost basis will not change – it will be the same as it was for the stock you contributed to the fund. We’ve covered this in detail above and we’ll lay out some examples in the next section, but we want to be clear about it: A primary goal of the fund is to defer capital gains taxes when you diversify your holdings.

When you sell your basket of stocks from the fund, capital gains will be calculated by subtracting the value of those assets from the cost basis of the stock you initially contributed.

What makes exchange funds effective for certain investors?

Exchange funds are for sophisticated investors with a concentrated stock position and a long-term time horizon for their investments. If you are all of those things, here are some simple examples of the diversification and tax advantages you might experience.

The benefits of tax deferral:

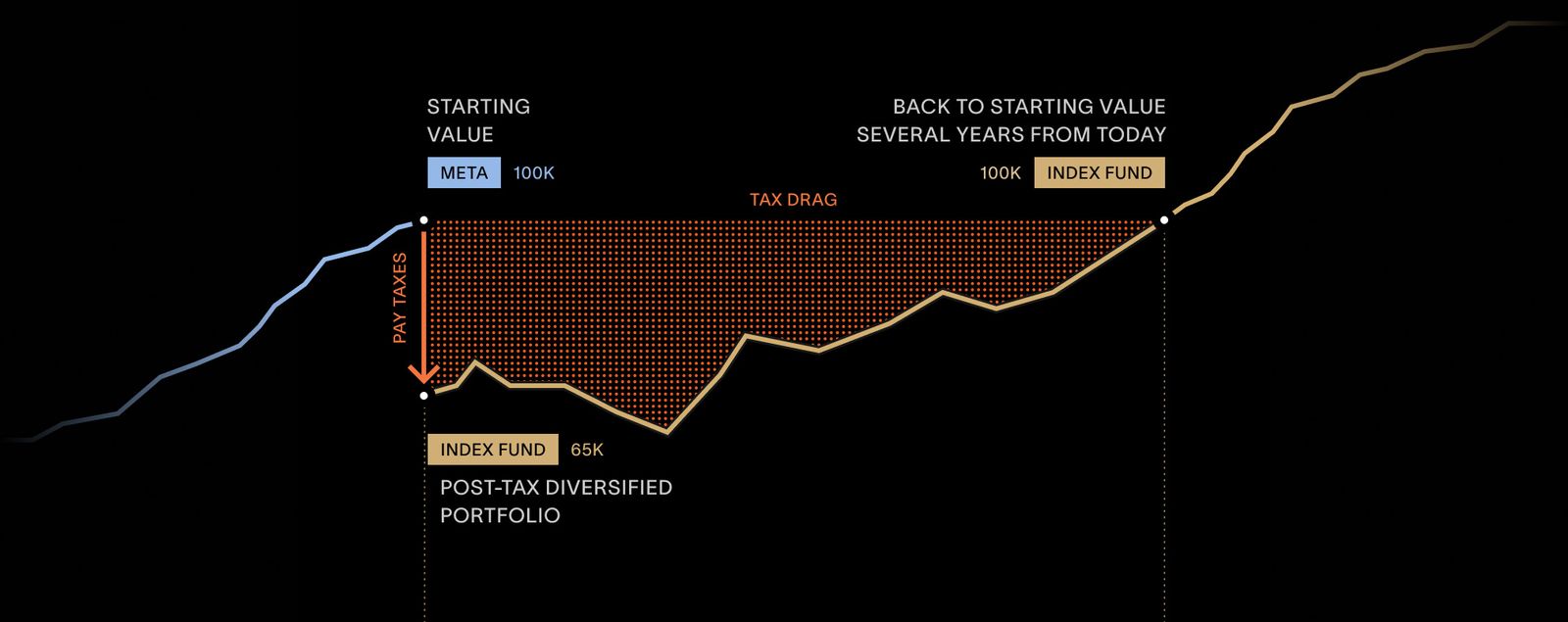

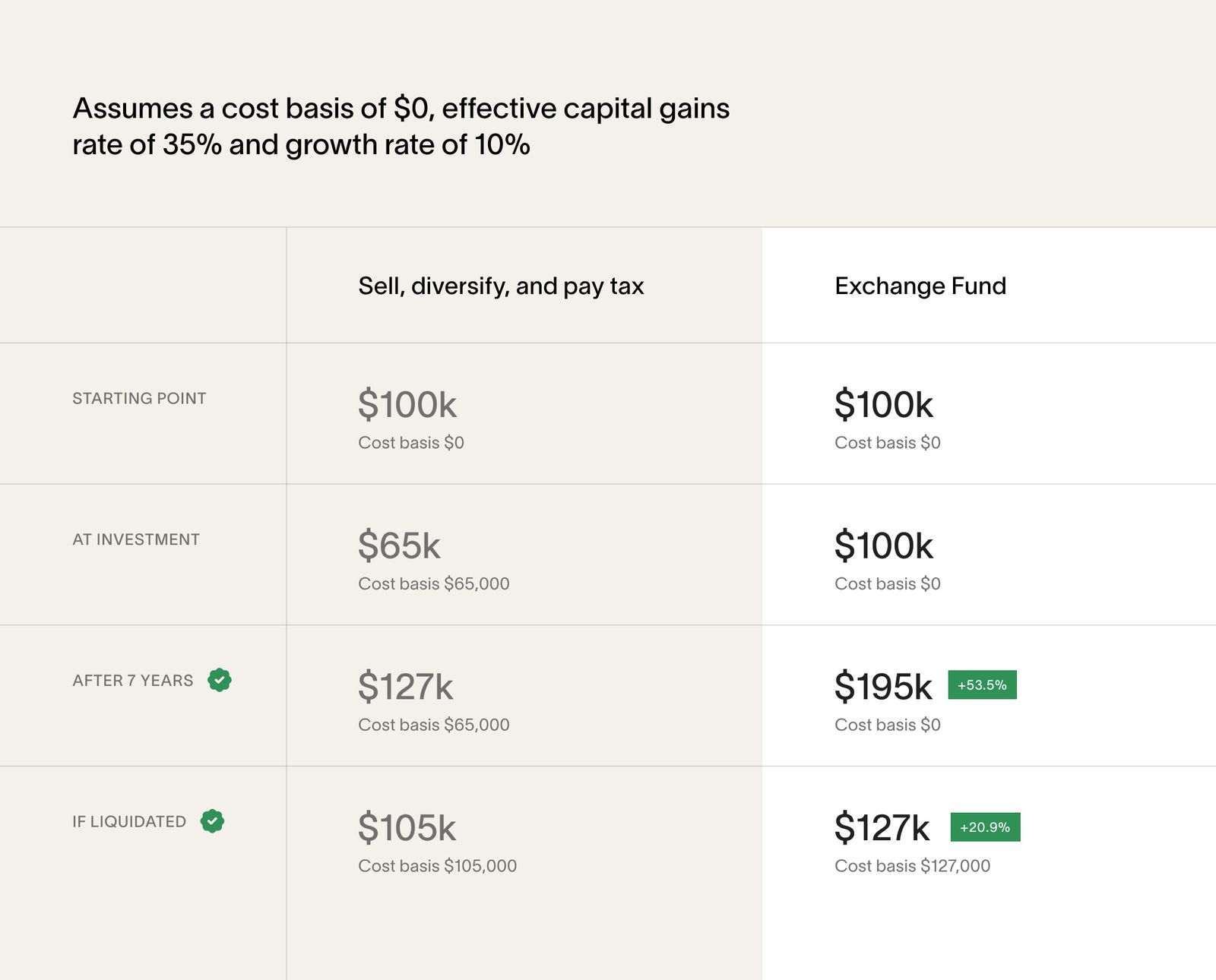

Exchange funds help defer taxes, but they don’t eliminate them. So is there still a financial benefit if you have to pay taxes eventually? Yes!

When you defer taxes, the money you would have paid in taxes remains invested and working for you in the market. It’s generally a good idea to take every dollar of tax deferral when you have an option because the leverage you gain by deferring taxes results in a compounding effect on returns. A smaller post-tax asset base can’t keep pace over time.

You can see how it works in this example:

If you want to play with the numbers, our exchange fund simulator does a great job explaining the compounding effect of tax deferral in a more interactive way.

The benefit of reducing concentration risk:

It can be a great feeling when you’re sitting on a pile of company stock that is increasing in value every day. However, it's a great feeling that comes with a downside: concentrated risk.

If your company takes a hit, your entire portfolio could suffer. As the legendary investor and philanthropist John Templeton once said, "The four most dangerous words in investing are: 'This time it's different.'" And he's right. It's always risky to put all your eggs in one basket, which is why it’s generally recommended that no one asset should make up more than 10% of your portfolio.

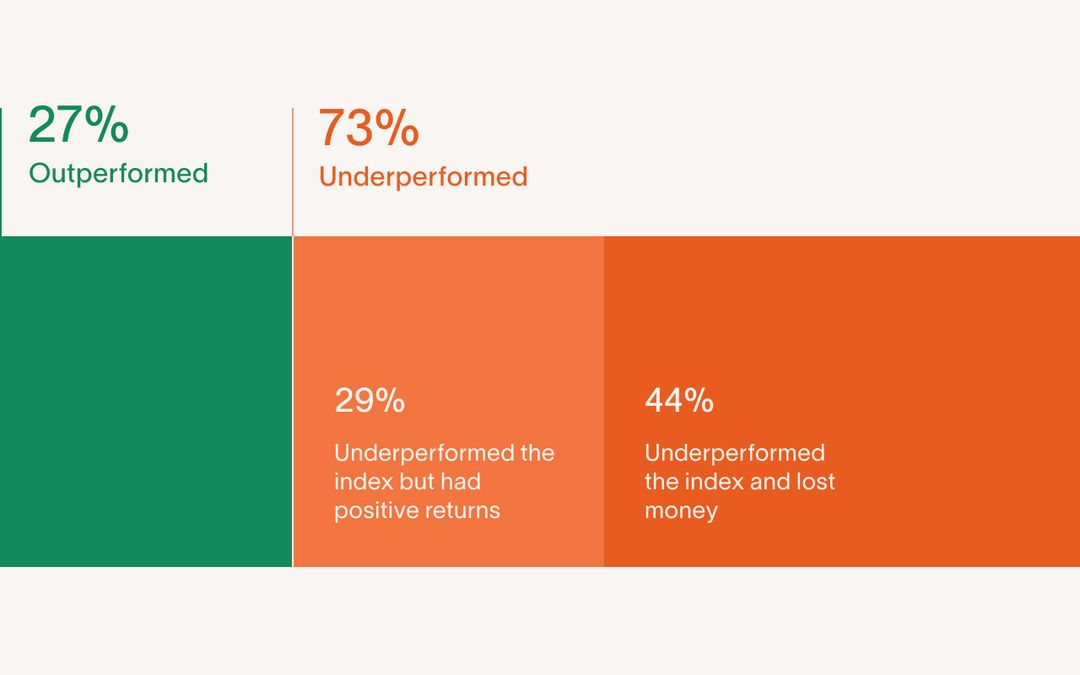

Moving out of a concentrated position may also improve your returns over time. While past performance is no guarantee of future returns, our analysis of the stocks in the Nasdaq-100 index found that almost three-quarters of the stocks in the index underperformed the index over a 22-year span and that 44% of those stocks actually lost money over that time period. On a risk-adjusted basis, very few stocks outperform the Nasdaq consistently. Other researchers have seen similar results when comparing index funds and individual stocks.

Individual Stocks vs. Nasdaq-100 | 2001 to 2023

Source: Cache, Bloomberg

This analysis is based on the returns of individual stocks in the Nasdaq-100 index from January 1, 2001, through September 25, 2023. Our analysis includes securities with different lifetimes in the index since securities are added and removed from the Nasdaq-100 over time. For the purposes of comparison, each security’s return is measured over its lifetime in the index.

Tax planning advantages:

Instead of being forced to liquidate your concentrated position when you still have high income and an unfavorable tax bracket, exchange funds provide diversification today and let you control when you liquidate your stock (if at all). This means you can liquidate small portions of your portfolio when you are in a lower tax bracket, or you can wait until you live somewhere with lower tax rates. By participating in an exchange fund, you don’t have to be concerned with concentration risk while you wait for a better tax window to open up.

Estate planning advantages:

Exchange funds can even provide significant estate planning benefits for certain investors. Upon your death, the current tax code allows your heirs to withdraw the diversified basket from a fund on a stepped-up basis. That means they wouldn’t have to pay any taxes for the appreciation of your stock at all. Of course, they might still be subject to estate taxes if your estate is larger than $13.61 million – the federal estate tax exemption in 2024.

What are the risks of an exchange fund?

Exchange funds can help you in lots of ways, but they’re not for everyone. In addition to the eligibility limitations discussed above, here are three other considerations for investors.

Liquidity considerations

Exchange funds are a long-term investment. Period. To take advantage of the tax benefits of an exchange fund, you are required to hold your shares for at least seven years. They simply do not offer daily liquidity like ETFs or mutual funds.

Tax considerations

There’s a chance that tax laws might change in the future, which may impact the favorable tax treatment of an investment in an Exchange Fund. While the benefits may be grandfathered in any new tax regulations, retroactive treatment is not guaranteed.

Investment considerations

Exchange funds are a passive investment vehicle designed to provide diversified exposure. They do not guarantee higher returns than their underlying stocks, and they are likely to fluctuate with market conditions. While exchange funds may be designed to track an index fund or ETF, it should also be noted that fund managers have limited ability to sell stock positions and rebalance the fund. Diversification reduces concentration risk, but it does not eliminate investment risk completely. It is still possible to lose principal when you participate in an exchange fund.

When should I use an exchange fund?

- Use them if your investment horizon is at least seven years.

- Use them if you have highly appreciated stock positions and you’d like to reduce your tax burden.

- Use them to reduce exposure and risk from a particular stock in your portfolio.

- Do not use them if you are likely to have a major liquidity need that depends on these stocks.

Examples of typical exchange fund participants

Assuming they are qualified investors and have a long-term investment outlook, these are three examples of the types of investors who may wind up finding an exchange fund useful:

The stock-earning employee

Joe has been working as a Software Engineer at Apple for 12 years. The stock grants he’s received have ballooned in value to make up a huge portion of his net worth. While he sells newer shares as soon as they vest, the AAPL stock he’s held for a long time still subjects him to concentration risk, and he’s essentially illiquid because of the stock’s 500% to 1000% increase in value. Joe can reduce his AAPL exposure by contributing his oldest shares to an exchange fund, diversifying his position without a giant tax bill.

The part-time angel investor

Mila is a VP of Operations who moonlights as an early-stage startup investor – mostly in companies her MBA classmates founded. She’s made smart bets that have paid off handsomely. She receives distributions from her early investments in Snowflake, Datadog, and Twilio, which have a negligible cost basis but aren’t eligible for qualified small business stock (QSBS). Instead of selling and diversifying out of her investments in SNOW, DDOG, and TWLO, Mila can contribute some of her shares to an exchange fund to reduce her portfolio exposure.

The timely stock picker

Jeevan has a passion for stock market investing and technology breakthroughs. In 2020, when he took delivery of his Tesla Model 3, he also invested $50K in TSLA, which has grown 800% since then – and become a large part of his portfolio. Jeevan can reduce his portfolio risk by contributing his TSLA shares to an exchange fund without throwing away years of growth in his shares.

How much should investors like these invest in an exchange fund?

When you contribute to an exchange fund, you don’t have to contribute all of your concentrated position. In fact, it’s quite common to use a variety of tools to diversify. It’s up to you (and any advisors you work with) to decide what your investment goals are and how to reach them. Consider an exchange fund to be one part of your overall strategy, and slot it in accordingly under the long-term investments column. We commonly see investors earmark 20-40% of their portfolios for the long term, but the amount can vary, depending on your financial circumstances.

How do you learn more?

If there’s one thing all the investors in the examples above have in common, it’s that they have a long investment horizon and a large holding in at least one stock. If that also describes you, then you might want to start looking at exchange fund providers or talking to advisors about your options.

Now that you know how an exchange fund works, you should be in a good position to have a productive conversation. We would be more than happy to answer any of your questions – whether they’re about The Cache Exchange Fund or about exchange funds more generally. Feel free to set up a quick call with our team, or take a closer look at our modern exchange fund products.

Material presented in this article is gathered from sources that we believe to be reliable. We do not guarantee the accuracy of the information it contains. This article may not be a complete discussion of all material facts, and it is not intended to be the primary basis for your investment decisions. All content is for general informational purposes only and does not take into account your individual circumstances, your financial situation, or your specific needs, nor does it present a personalized recommendation to you. It is not intended to provide legal, accounting, tax or investment advice. Investing involves risk, including the loss of principal.