Managing tax drag when diversifying your portfolio

What you'll learn

We recently conversed with a seasoned Facebook engineer who was contemplating the optimal method to diversify his META stocks. Typically, he would sell the stocks to acquire a diversified ETF, but he hadn't considered tax drag. It's a concept that both he and you must grasp to make fully informed investment choices.

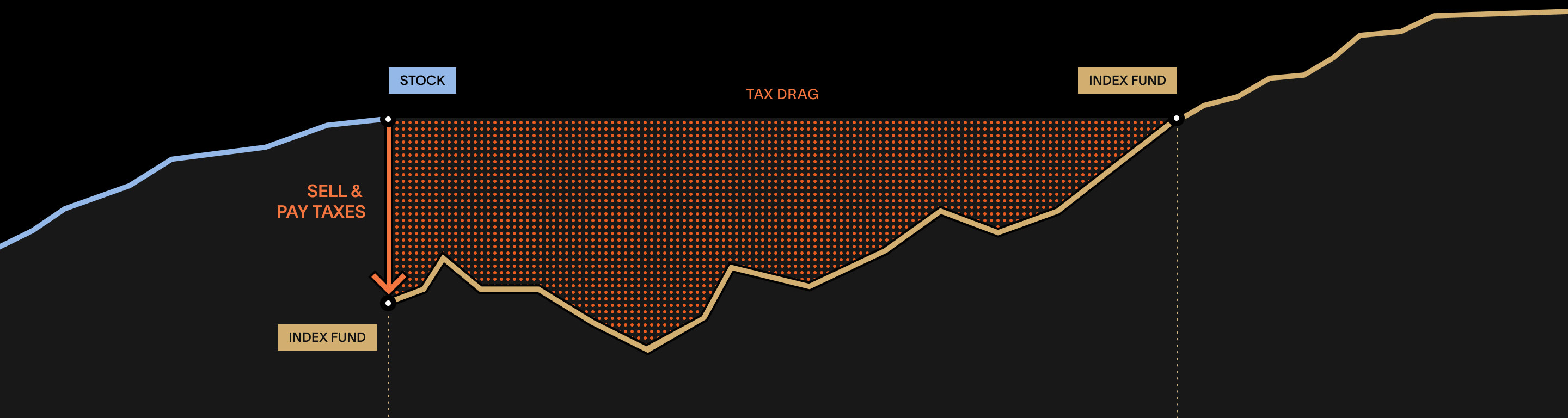

When you possess a stock that has significantly appreciated in value, you may encounter a difficult decision. Holding onto your position exposes you to the concentration risk of having a substantial portion of your net worth invested in a potentially volatile stock. However, selling that stock to diversify your portfolio can entail paying capital gains taxes of 35% or more.

It can require years for a portfolio to recuperate from the capital gains taxes forfeited when you sell and diversify a concentrated position. This illustration assumes a 35% effective capital gains tax rate when selling appreciated META stock to mitigate concentration risk.

Benjamin Franklin said “nothing can be said to be certain, except death and taxes.” Certain wealth managers might advocate for combining the two approaches and deferring taxes until later in life. Nonetheless, many individuals require funds or opt to diversify their investments during their lifetimes. When you pay taxes to transition from one investment to another, you have fewer post-tax funds available for market investment, and your capital accumulates at a slower pace on an absolute basis. This exemplifies the impact of tax drag.

What is tax drag?

Tax drag refers to the continual adverse effect that paying taxes can exert on an investor's overall returns. It arises when transitioning from one investment to another and triggering a taxable event, as illustrated by the Facebook engineer we mentioned earlier.

When taxes are paid, the principal available for investment decreases. This is akin to erasing years of growth in your portfolio. As your investment compounds over time, the returns are diminished because there is less principal available for compounding.

In certain situations, tax drag can be mitigated if taxes can be avoided altogether, deferred for payment at a later time, or offset by capital losses. We'll delve into these scenarios in detail below.

An example of tax drag

To witness tax drag in action, let's revisit the scenario of the early Facebook engineer we mentioned at the outset.

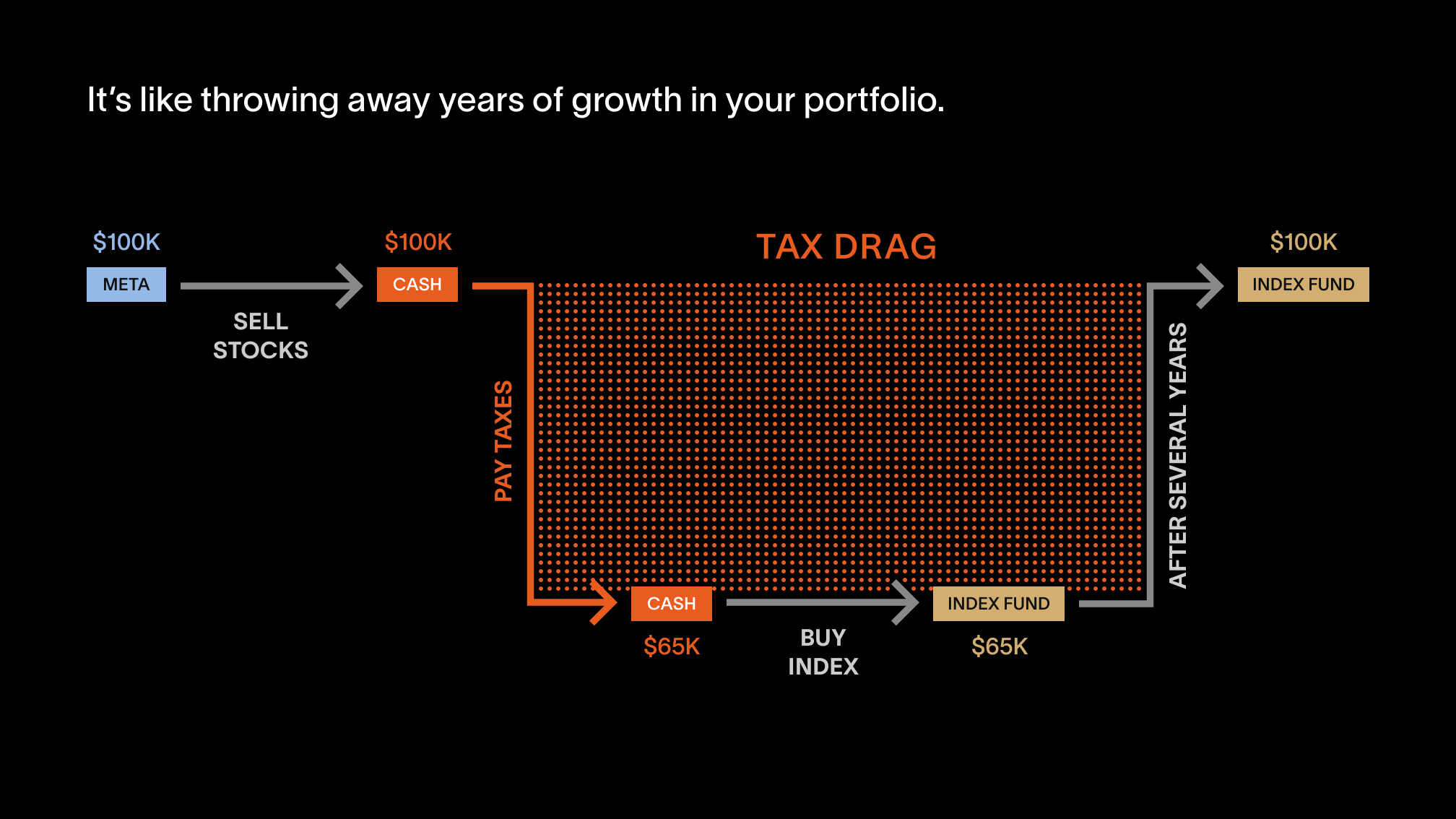

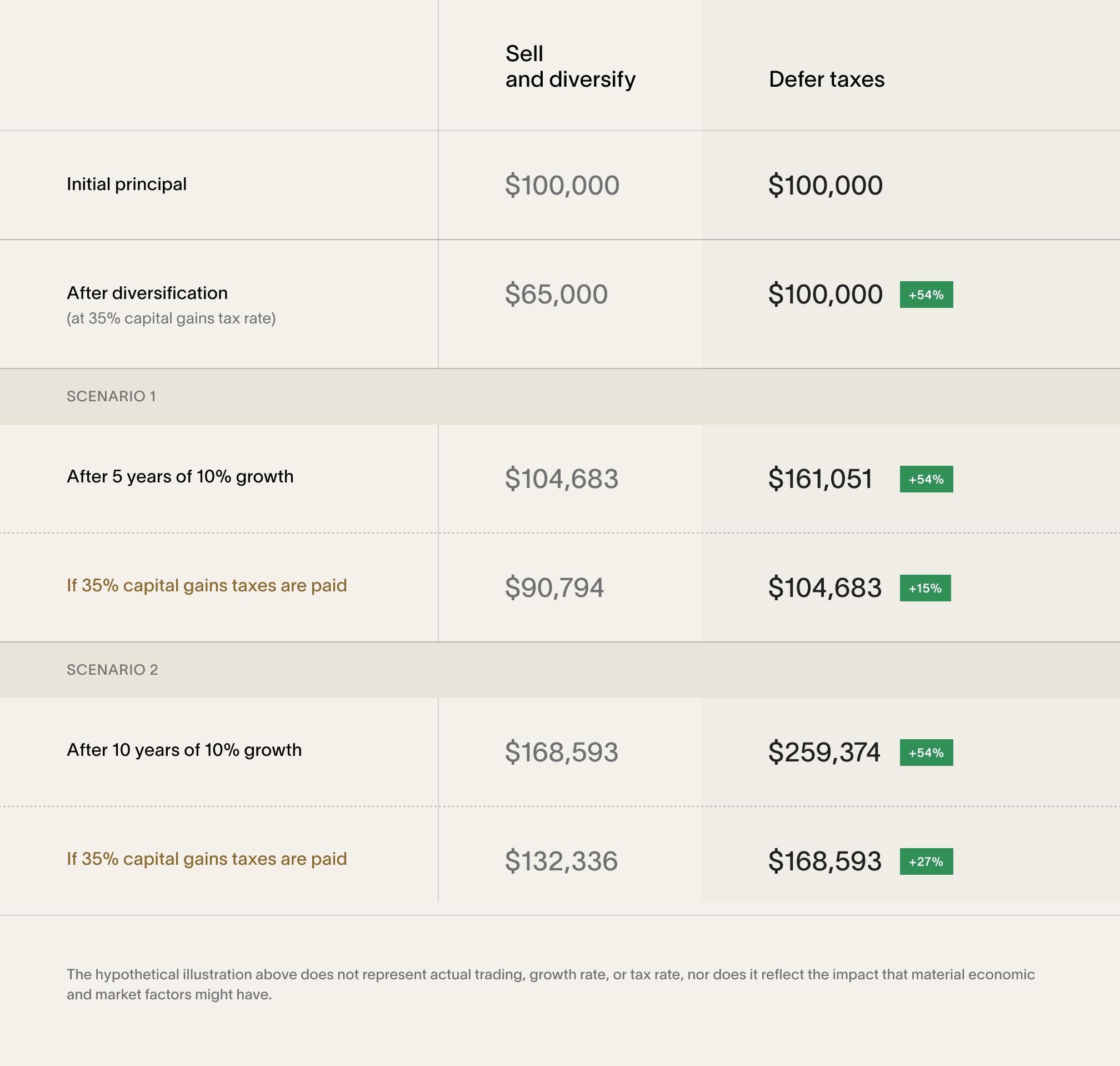

The engineer is a high earner in California, implying that he could face an effective capital gains rate of 35%. With a negligible cost basis for the META stock earned as compensation, every $100K in META that he sells and diversifies would incur $35K in taxes.

If he reinvested the remaining $65K in a diversified fund, it would require almost five years to return to his initial position of $100K, assuming an average annual return of 10%.

It can take years for a portfolio to recover from the capital gains taxes forfeited when selling and diversifying a concentrated position. This scenario assumes a 35% effective capital gains tax rate.

Conversely, a dollar of tax deferred is a dollar that continues to work in your favor. Over time, this can accumulate into a significant advantage, even if you ultimately pay all the taxes later on.

If the Facebook engineer managed to diversify his holdings without resorting to a sale, his $100K investment would be valued at 54% more than in the scenario where he paid taxes to diversify—assuming the same 10% growth rate over five years.

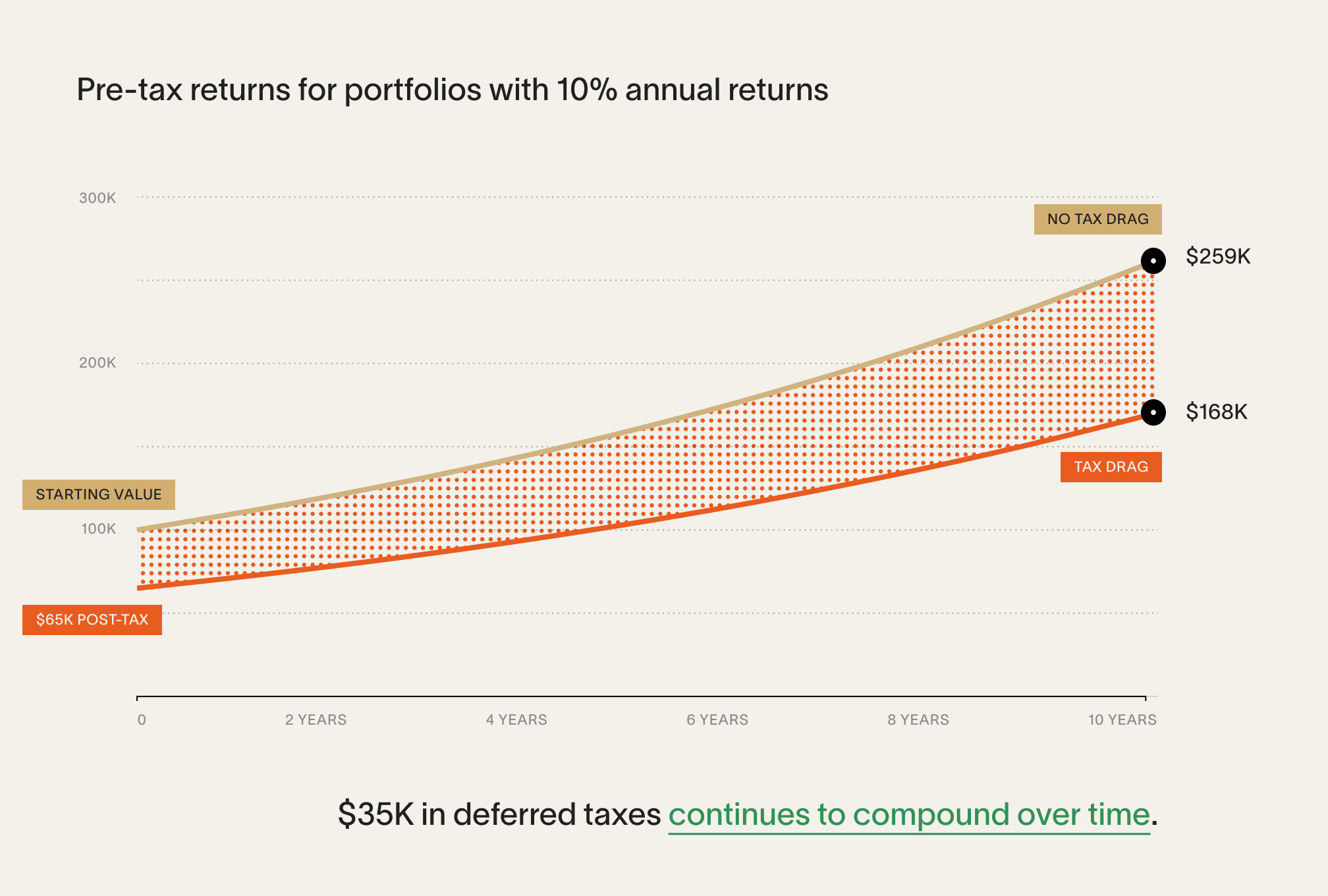

As demonstrated in the example above, the influence of compounding returns would persist over time for the Facebook engineer. If he delayed selling and paying taxes on his tax-deferred portfolio for 10 years, his post-tax returns would be nearly 27% greater than if he paid taxes upfront. The impact of compounding interest becomes evident when plotting the 10% returns over time on a chart.

The hypothetical example above does not depict actual trading or reflect the influence of significant economic and market factors. It assumes a 10% annual return; however, it's important to acknowledge that all investments carry risks.

Calculating tax drag

Estimating the potential tax drag on your portfolio may require some spreadsheet expertise, which is why we developed a tax drag calculator to simplify the process of understanding your situation. If you have information regarding your cost basis and the approximate value of the stock you own, explore our simulator for insights.

The calculator computes and contrasts the various outcomes if you opt to diversify and sell or participate in a tax-deferred exchange fund. The outcome with an exchange fund should resemble the example we presented earlier; however, employing figures that approximate your circumstances can underscore the extent to which tax drag could potentially impede your long-term performance.

How to optimize tax drag

Tax drag doesn't have to be an unavoidable reality!

Let's clarify: Taxes are almost always triggered when you sell your assets (e.g., to raise cash for purchasing a house or other financial needs). However, when you are selling one investment to acquire another, tax drag can be optimized and should be a significant consideration.

The tax code offers several methods to optimize your portfolio. Like-kind exchanges (such as exchange funds), tax-loss harvesting, gifts, and charitable trusts all offer avenues to prevent taxes from eroding your principal. Here are some brief insights into each approach:

-

Exchange funds

Not to be mistaken for ETFs, exchange funds aggregate stocks from various investors to form a diversified fund. Your stock contribution isn't taxed, and after a seven-year period, you can withdraw a diversified pool of stocks from the fund without incurring taxes. The example provided essentially outlines the tax-deferred performance of an exchange fund. Exchange funds are now accessible to investors with as little as $100,000 to invest. Explore the Cache Exchange Fund to learn more about how they mitigate tax drag.

-

Tax-loss harvesting

An investment advisor can assist you in establishing a separately managed account designed to systematically sell portions of your appreciated stock position. The proceeds are then reinvested in a diversified basket of stocks. As these stocks fluctuate in value, capital losses are recognized, offsetting some of the capital gains in your portfolio. It's crucial to recognize that it can require significant capital losses to offset highly appreciated stocks, as it operates on a dollar-for-dollar basis.

-

Choose a new path

When you participate in a retirement plan, you're circumventing tax drag by contributing pre-tax income. While your IRA or 401(k) cannot assist you in deferring taxes on stock you already own, if you're contemplating long-term strategies, you may leverage these accounts to acquire stock with the potential for significant appreciation. Upon retirement, this could translate into a reduced tax burden (subject to the tax status of the investment account). For instance, VC Peter Thiel famously utilized his Roth IRA to purchase $1700 worth of Paypal stock at $0.001 per share. Today, that stock is valued at several billion dollars!

-

Charitable giving

Certain charitable giving vehicles enable you to donate stocks to charitable causes without triggering capital gain taxes initially. Additionally, you'll receive a tax deduction that can be utilized in other areas of your portfolio. Depending on how they're structured, you can diversify the holdings and even generate income from the stocks you've donated during your lifetime. These vehicles are known as Donor Advised Funds (DAF) and Charitable Remainder Trusts (CRT).

However you decide to proceed, it's certainly worthwhile to explore your options. If you're contemplating diversifying and selling, you're on the right track. Take the additional time to assess the potential tax drag on your portfolio, and if you're uncertain about your options, consult with an advisor to determine the most effective ways to achieve your investment goals.

More about exchange funds

Having experienced a situation akin to the Facebook engineer we've discussed, we conducted the same research you're undertaking today. We firmly believe that like-kind exchanges facilitated by exchange funds represent a potent solution for evading tax drag. In fact, our conviction in this belief is so strong that we established this company, Cache, to make them accessible to individual accredited investors for the first time.

To qualify for a modern exchange fund like the one Cache offers, you must meet the SEC's definition of an accredited investor. Additionally, you need to invest a minimum contribution of $100,000, demonstrate financial stability to commit for at least seven years, and acknowledge the associated risks, including limited liquidity, investment constraints, and the potential for changes in tax laws. While diversification mitigates concentration risk, it doesn't entirely eliminate investment risk. Loss of principal remains a possibility when participating in an exchange fund.

For a comprehensive understanding of exchange funds, you can delve deeper into the topic. Alternatively, you can explore how direct indexing compares to exchange funds. We're also available to address any questions you may have if you're inclined to share more about your situation!

Material presented in this article is gathered from sources that we believe to be reliable. We do not guarantee the accuracy of the information it contains. This article may not be a complete discussion of all material facts and is not intended as the primary basis for your investment decisions. All content is for general informational purposes only and does not take into account your individual circumstances, financial situation, or your specific needs, nor does it present a personalized recommendation to you. It is not intended to provide legal, accounting, tax or investment advice. Investing involves risk, including the loss of principal.